Home / News

-

by Deloitte Ireland LLP 09 Jun 2026

by Deloitte Ireland LLP 09 Jun 2026Housing crisis and cost of living reshaping lives of Ireland’s Gen Zs and millennials

Learn More -

-

by Institute of Directors Ireland 08 Jun 2026

by Institute of Directors Ireland 08 Jun 2026Accountability in Action: How Honest Evaluation Shapes Governance

Learn More -

by Mercedes-Benz Ballsbridge 06 Jun 2026

by Mercedes-Benz Ballsbridge 06 Jun 2026The New Mercedes-Benz CLA: Intelligence, Efficiency, and a New Era of Electric Mobility

Learn More -

IFSC News 05 Jun 2026

IFSC News 05 Jun 2026Euronext welcomes the entry into application of the Listing Act and launches a new admission framework

Learn More -

-

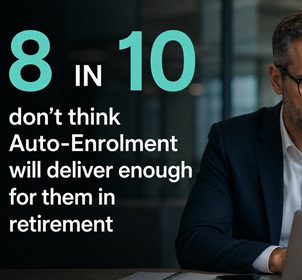

IFSC News 04 Jun 2026

IFSC News 04 Jun 20268 in 10 don’t think Auto-Enrolment will deliver enough for them in retirement

Learn More -

by Board Excellence Limited 03 Jun 2026

by Board Excellence Limited 03 Jun 2026Optimising the value the Board adds to the CEO and Executive Team

Learn More -

by Deloitte Ireland LLP 03 Jun 2026

by Deloitte Ireland LLP 03 Jun 2026Irish Aircraft Leasing Industry Remains Extremely Resilient Despite Fuel Turbulence

Learn More -

-

IFSC News 03 Jun 2026

IFSC News 03 Jun 2026Social Media Has 2nd Biggest Influence On Young People Choosing Financial Advisors

Learn More -

by Coopman Search and Selection 02 Jun 2026

by Coopman Search and Selection 02 Jun 2026Dublin Financial Services Talent Market Update – H1 2026

Learn More